All You Need to Know About Title Insurance: Protecting Your Ownership

When you buy a home, you aren't just buying the bricks, mortar, and the yard—you are buying the Title to the property. The title is your legal right to own and use the land.

But what happens if someone from the past claims they still own a piece of it? That’s where Title Insurance comes in.

What is Title Insurance?

Title insurance is a policy that protects you (and your lender) from financial loss due to defects in a property's title. Unlike car or health insurance, which protects you from future events, title insurance protects you from past events that occurred before you even owned the home.

The Two Types of Policies

When you close on a home, there are actually two different policies in play:

Lender’s Policy: If you are financing your home, your bank will require this. It protects their investment in the property. It only covers the amount of the loan and decreases as you pay your mortgage down.

Owner’s Policy: This is optional but highly recommended. It protects your equity and your right to live there. It lasts as long as you or your heirs own the property.

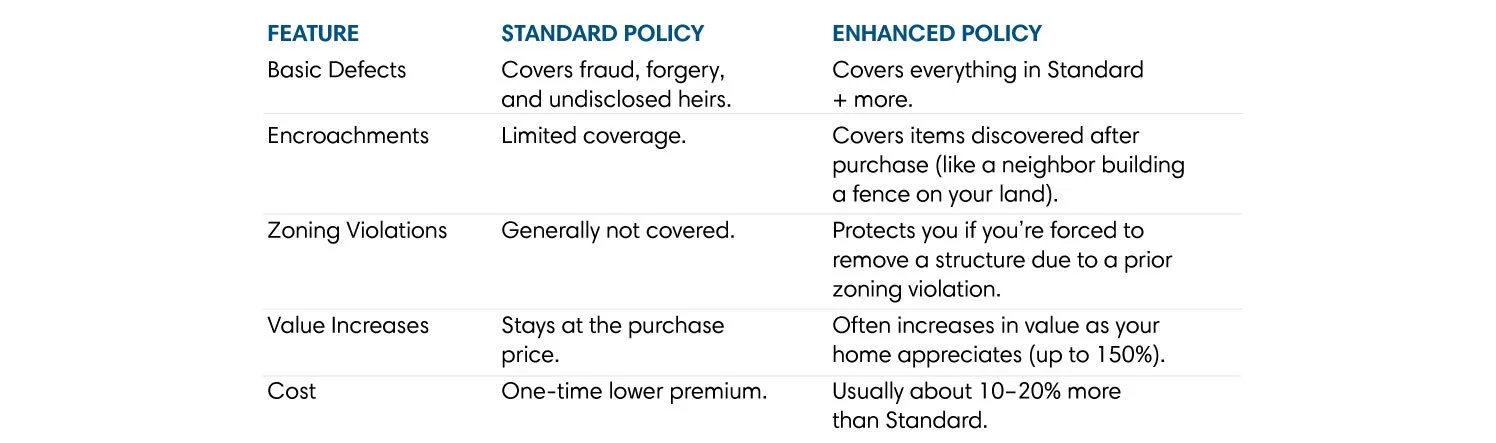

Standard vs. Enhanced Coverage: What’s the Difference?

Most title companies offer two "flavors" of owner's title insurance. Here is how they generally compare:

The Cost Structure: Local Customs in MD & DC

Title insurance is unique because there are no monthly premiums. You pay a one-time fee at closing.

Who Pays? In our local jurisdictions of Maryland and the District of Columbia, the cost of title insurance (both the Lender’s and the Owner’s policies) is almost always in the buyer’s column. Because this is a significant closing cost, it’s important to budget for it early in the process.

The "Re-issue Rate": If the seller has owned the home for a short period (usually 10 years or less) and can provide their old policy, you may be eligible for a Re-issue Rate. This is a significant discount because the title search doesn't have to go as far back into history. Always ask your title company if the property qualifies for this rate!

Main Issuers in the United States

While you will likely work with a local title agency, your actual insurance policy is usually backed by one of the "Big Four" who dominate the U.S. market:

Fidelity National Financial

First American Title

Old Republic National Title

Stewart Title

Does Title Insurance Lose Value?

No! In fact, it’s the opposite. An Owner’s Policy remains in effect for as long as you or your heirs own the property. It never expires. If you choose an Enhanced Policy, the coverage amount often grows as your home value increases, ensuring you are protected for the current market value, not just what you paid ten years ago.

Why Should a Buyer Get It?

Even the most diligent title search can miss "hidden" hazards, such as:

A previous owner’s unpaid child support or taxes.

A long-lost heir claiming they inherited the house in a missing will.

Mistakes in the public records or forged signatures on previous deeds.

Without an owner's policy, you would be responsible for the legal fees to defend your ownership—and you could potentially lose your home and your down payment.

The Bottom Line

Title insurance is the ultimate "set it and forget it" protection. For a one-time fee at closing, you ensure that your "home sweet home" stays yours forever.